Overview

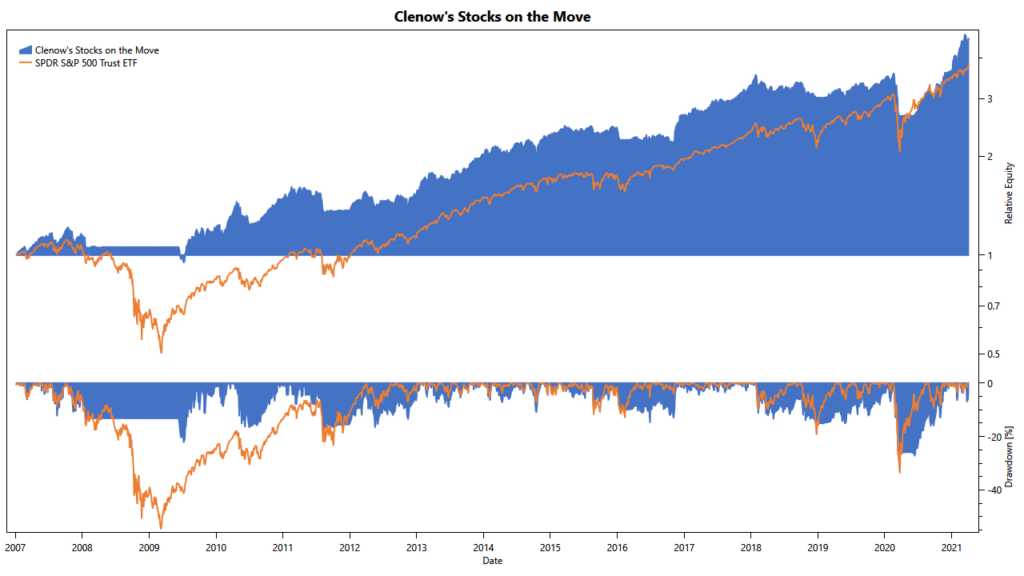

When it comes to books about quantitative trading, Andreas F. Clenow’s Stocks on the Move is one of our favorites. The book introduces a simple momentum-based strategy trading S&P 500 stocks. But describing the strategy rules is only a small part of the book. Much more importantly, the book walks through the strategy’s components, explains each feature’s reasoning, and reviews the strategy’s performance over 15 years.

Armed with this knowledge, the implementation of the strategy is straightforward. We open-sourced the strategy’s source code.

Naturally, hopes are high that this strategy would vastly outperform the market – but unfortunately, it doesn’t. All the components are in place, the proper analysis is done, but where the rubber meets the road, something is missing. We see the strategy’s potential in periods of nice bull runs… until it loses most of its edge in sudden downturns. For TuringTrader.com, we created two proprietary variants of this strategy, Stocks on the Loose and Stocks on a Stroll, by fixing the few things that are broken in Clenow’s original work.

Risk Management

Clenow goes through great length explaining the fixed fractional position sizing and its benefits. And we fully agree with his reasoning. However, we believe that he omitted talking about some important edge cases. We acknowledge that each position represents a fixed dollar amount of risk with the proposed position sizing. Clenow suggests we keep allocating capital along our ranked list of stocks until we assigned all capital. There are two situations where this becomes problematic:

- Volatility is very low. Under these circumstances, stock positions can get much larger. We may run out of capital early and open fewer positions than we would want to. As a consequence, we lose diversification and add unnecessary concentration risk to our portfolio.

- Volatility is very high. Under these circumstances, stock positions get much smaller. If we were to allocate all capital, we would open many more positions than usual. As each position represents one unit of risk, this means that our total portfolio risk increases accordingly.

This second issue is especially troubling. The chart above shows how Stocks on the Move invests in about 20 stocks in calm markets. With the given position size of 10 basis points, that results in risking about 2% of the portfolio value each day. But as a precursor to market downturns and before the market regime filter forces the strategy to divest from the stock market, Stocks on the Move has often taken on twice that risk. Assuming that the whole stock market becomes highly correlated in times of stress, the risk-parity approach alone does not buy us any improvement over the much simpler equal-capital position sizing.

Stocks on the Loose and Stocks on a Stroll address both of these issues. For once, the strategies limit the maximum percentage of capital that can be allocated to a single stock. In doing so, the improved money management enforces a minimum level of diversification. Further, our strategies limit the maximum portfolio risk. Our improved money management gracefully scales back position size and limits exposure in nervous markets with high volatility. As a result, Stocks on the Loose and Stocks on a Stroll become less prone to excessive losses.

Idle Capital

Clenow’s strategy only holds idle cash when the market regime filter indicates bearish conditions. With our modified money management, we begin to gradually exit the stock market much earlier than Clenow’s strategy. Consequently, we need to think a little harder about alternative ways of investing that capital.

Our Stocks on the Loose and Stocks on a Stroll strategies use our Buoy strategy instead of holding idle cash. Buoy is an expansion of Heine’s Bond Trading Model that uses a combination of trend-following and macro-economic cues to find bonds with the highest returns. The strategy was specifically designed with rising yield rates in mind, as experienced in 2022. The chart above shows how the addition of a bear-market strategy nicely fills in the recession period during which Stocks on the Move stayed flat.

Having a solid alternative to stock investments allows us also to put a completely different spin on the original strategy. Stocks on a Stroll invests only about half of its capital in stocks and allocates the remainder to Buoy. As a result, Stocks on a Stroll no longer aims to produce aggressive growth but comes with a docile and bond-like personality even though it is based on the exact same code and principles as Stocks on the Loose.

Market Regime Filter

Clenow suggests a simple 200-day moving average filter to detect bearish market conditions. This simple method is appropriate for a book, but we feel that we can and should do better. Since we have Market Vane in our arsenal, we decided to retrofit the strategy with our advanced market regime indicator.

The results of this change are very noticeable. Because Market Vane exits the stock market much faster than the 200-day moving average, we can avoid sudden drawdowns as seen in 2008 or March 2020. And thanks to not holding idle cash but investing in Bonds-NOT, we are even able to make some money during these risk-off periods.

Trading Universe

Clenow’s strategy trades the S&P 500, which is undoubtedly a good universe. But we have multiple reasons why we wanted to change that.

- Volatility: Momentum strategies rely on predictable momentum with as little volatility as possible. In our opinion, blue-chip stocks from the S&P 100 better fit that bill then many of the stocks found towards the bottom of the S&P 500.

- Liquidity: The stocks we find at the bottom of the S&P 500 have about 1/100th of the liquidty we find at the top. We are concerned that daily trading volumes around 15 million dollars might not be enough. You can read more about this in our background article about market liquidity.

- Simulation Time: The universe is relatively large. Between 1990 and 2021, this universe included more than 1,200 constituents, leading to long simulation times. In contrast, the S&P 100 universe only had about 230 constituents, resulting in approximately six times faster backtests. While this should not be the deciding factor for a universe, it certainly is an added bonus.

Wrap Up

All of these changes are relatively simple. Stocks on the Loose and Stocks on a Stroll share about 90% of the code with the original Stocks on the Move implementation. And yet, the results are dramatically different.

The direct comparison of the equity charts shows how Stocks on the Loose produces much higher returns while at the same time substantially reducing the downside. And the risk/ return chart shows how Stocks on the Loose beats Clenow’s original with approximately twice the returns at half the risk.

So if you’ve been disappointed after first implementing Clenow’s strategy, don’t be. Stocks on the Move is a great book describing a solid strategy. All it needs are a few tweaks to turn it into something that fits the bill nicely.